On 2nd February 2026 the Bank of England’s Deputy Governor Sarah Breeden said in a speech at City & Financial Payments Regulation and Innovation Summit 2026: “Competition from an extra payment option could bring … costs down. And in the context of a challenging and changing cyber and operational risk environment, it could provide a degree of extra resilience in the UK payments landscape, as an additional payment rail on the rare occasion of operational disruption to existing rails.”

On 19th February 2026, Piero Cipollone, Member of the Executive Board of the ECB stated that “.. there is one domain where Europe’s sovereignty is already under pressure: retail payments.

The role of cash – our sovereign means of payment – is declining as digitalisation accelerates. And almost two-thirds of card-based transactions in the euro area are carried out by non-European companies. Thirteen euro area countries depend entirely on international card schemes. And for those countries that have a domestic card scheme or national scheme for e-commerce payments, like Italy, data show that these schemes are losing market share across Europe.”

What does a Solution to the Sovereign Payment Rail Challenge Look Like?

The UK’s Retail Payments Infrastructure Board (RPIB) was established by the Bank of England in 2025 to design and deliver the UK’s next-generation retail payments infrastructure, and whilst the detailed design is not yet available, the following requirements have been identified as being particularly relevant (with links where available).

|

Dispute / Chargeback AI Fraud Offline Capability Sovereign Residency POS Multi-Rail Programmable Payments |

How can Trusek help address Independent Sovereign Payment Rail Requirements?

Trusek has developed a platform called the Unified Payment System (UPS). The UPS was designed to enable regulated financial institutions to implement an Independent Payment Rail facility that processes payments through a stand-alone platform which supports a range of payment types and use cases.

An internal Capability Alignment Summary comparing the Bank of England’s published Retail Payment Infrastructure requirements to existing UPS capabilities indicates that approximately 65% of the Sovereign Infrastructure Requirement already aligns to developed technical capabilities and includes: –

-

- A2A rail architecture,

- real-time settlement with transaction finality,

- node-based network topology,

- API-first integration,

- configurable compliance

- AML rule engine,

- multi-currency/FX capability,

- enterprise-grade security controls.

Following is a high-level summary of the UPS Platform’s capability: –

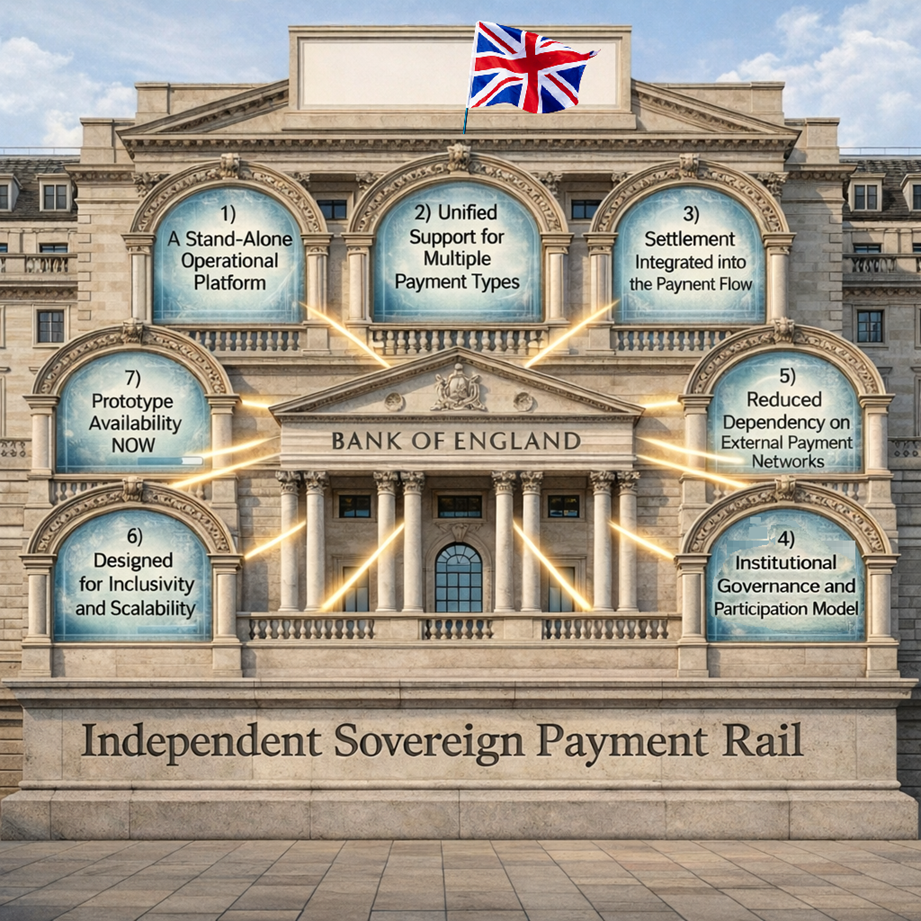

1) A Stand-Alone Operational Platform

UPS operates as a dedicated payments environment rather than an overlay on top of existing legacy card (Visa & MasterCard) or Correspondent systems. This allows participating institutions to:

-

- Process payments within a unified ecosystem

- Manage access, permissions and institutional participation

- Apply their own compliance rules and governance standards

- Maintain operational oversight within a controlled framework

Because the platform is purpose-built for regulated institutions, participation is structured, transparent and aligned with regulatory expectations.

2) Unified Support for Multiple Payment Types

A sovereign payment rail must handle more than one type of transaction. UPS is designed to support a broad range of payment use cases within the same environment, including:

-

- Account-to-account transfers

- Merchant payments

- Payment requests

- Direct debit-style arrangements

- Cross-currency transactions

- Settlement and reconciliation functions

Instead of building separate rails for each use case, institutions can deliver them through a single unified model.

3) Settlement Integrated into the Payment Flow

UPS integrates settlement into the transaction process. This reduces operational friction and improves certainty for participants.

For regulated institutions, this means:

-

- Improved liquidity visibility

- Reduced reconciliation complexity

- Fewer intermediary dependencies

- Greater control over payment finality

All of which supports the objectives of a sovereign rail, resilience, clarity and operational control.

4) Institutional Governance and Participation Model

UPS enables banks and regulated entities to operate cooperatively while maintaining independence. The model supports:

-

- Institution-led participation

- Clearly defined roles (network partners and transaction partners)

- Configurable fee structures

- Built-in compliance and rule management

This allows jurisdictions or banking groups to establish a payment rail aligned to their own regulatory and policy priorities.

5) Reduced Dependency on External Payment Networks

By enabling payments to be processed within a dedicated environment, UPS reduces reliance on external card schemes or multi-layer correspondent chains. For sovereign implementations, this supports:

-

- Greater strategic autonomy

- Clearer operational accountability

- Simplified network architecture

- Enhanced oversight of payment flows

6) Designed for Inclusivity and Scalability

A sovereign rail must be capable of growth. UPS is structured so that value exists from the first connected institutions and expands as participation increases. This enables:

-

- Early deployment in defined markets

- Gradual scaling across institutions

- Inclusion of smaller regulated participants

- Sustainable network growth

7) Prototype Availability and Timeline Acceleration

Trusek’s UPS platform has already been developed and is available for immediate prototype deployment.

While it does not currently deliver 100% of the full sovereign requirements “out of the box,” the platform provides a substantial foundation upon which those capabilities can be progressively enhanced.

Early adoption, even purely for structured prototype and evaluation purposes has the potential to significantly compress and accelerate overall programme timelines.

Based on current industry understanding, the anticipated roadmap for a new sovereign payment rail is:

2026–2027: Design and procurement

2027–2029: Build, pilot and commercial onboarding

2029–2030: Phased migration and scaling

By leveraging an already operational platform, elements of the design, build and pilot phases could run in parallel rather than sequentially. This may accelerate proof-of-concept validation, reduce procurement risk, shorten time-to-learning, and bring forward tangible progress by 12–24 months.

UPS therefore offers not just a technology solution, but a practical pathway to earlier market validation and programme de-risking.

For more information, please contact us. You can reach us by email at hello@trusek.com or my phone by calling +44 (0) 207 048 0470 or by clicking the Get in Touch or Contact Us links and buttons on the website.